Q My oldest daughter will be starting high school in the fall. Recently our local school board announced it would be changing principals at various schools, and my daughter’s school is getting a principal transferred from another high school. I have several friends who work for the school board, so I asked one about this man. The response I got was half-hearted praise, but I felt like there was something she wasn’t telling me. I pressed the issue, and she told me there is a not-well-kept secret about this principal.

Apparently, years ago, when he was a teacher, he had a sexual relationship with a student at the school where he was teaching. When some of the other teachers learned about this, they reported it to the principal and board office. However, they were shut down and told not to pursue this any further. They were given various reasons, ranging from the fact the victim had not come forward, and this would have a major impact on her if this came out, to the school board not wanting the controversy, to the fact this teacher was a very good football coach and this would hurt the team.

Richard Bilkszto died by suicide this July, his lawyer said in a statement. Earlier this year, he filed a lawsuit against the Toronto District School Board alleging he was bullied and harassed during anti-racism training sessions in the spring of 2021.Handout

So many bad things can happen at work. Among the worst is being subjected to racist treatment. Harassment of any sort is up there too. The workplace should be a safe space. The lucky among us think of our jobs as a vocation, and our place of employment as a sort of second home.

Another one of the worst things that can happen at work is being wrongly accused of being a racist. Such an accusation – even if it is challenged, disproved, dismissed – is a scarlet R that can be career-ending. Perhaps even life-ending, as we have learned with the tragic case of former Toronto District School Board principal Richard Bilkszto.

Mr. Bilkszto, according to a statement released by his lawyer, died by suicide this month at the age of 60. Earlier this year, he had filed a lawsuit against the TDSB (which has not been tested in court) alleging he was bullied and harassed during anti-racism training sessions in the spring of 2021 conducted by an outside consultant, KOJO Institute founder Kike Ojo-Thompson. This happened after Mr. Bilkszto – who used to teach in Buffalo – challenged the workshop leader’s statement that Canada was more racist than the U.S., according to the statement of claim.

Mr. Bilkszto said it would have done “an incredible disservice to our learners” to return to the classroom the next day and teach that Canada “was just as bad as the United States.”

The Toronto Star reports that this comparison was not initiated by Ms. Ojo-Thompson, but by other participants. And that her comment was a personal one about the racism she had experienced in Canada versus her time in the U.S.

Mr. Bilkszto’s lawsuit alleges that he was implicitly referred to as a racist and white supremacist, and that senior TDSB staff did not stop the harassment.

The Minister of Education is now investigating. Ontario’s Workplace Safety and Insurance Board previously found that the facilitator’s conduct was “abusive, egregious and vexatious, and rises to the level of workplace harassment and bullying.”

Of course, suicide is a complex matter. It is impossible for an observer to know exactly why Mr. Bilkszto ended his life. We don’t know about other possible factors, or whether this incident was directly responsible.

His lawyer, Lisa Bildy, says it was. “Unfortunately, the stress and effects of these incidents continued to plague Richard,” her July 20 statement read. “Last week he succumbed to this distress.”

The Ontario Principals’ Council said it was “deeply saddened and disturbed” by Mr. Bilkszto’s death: “Employers have an obligation to provide a safe working environment and to protect their staff from bullying and harassment.” That did not appear to happen for Mr. Bilkszto. And you can bet that it’s not happening for other people wrongly accused in other workplaces, in organizations that are themselves terrified to be labelled as racist.

Employers have an obligation to fairly investigate, to not make an example of someone without evidence, and to offer support for people who have suffered as victims of discrimination or harassment, as well as those accused. Rather than being automatically shunned by their peers and bosses, the accused should also be considered during this difficult process; they may require mental health support. Charged with being racist bullies, they themselves might be victims of bullying.

Mr. Bilkszto appears to have done the right thing: he spoke up, informed by his many years as an educator and what he had seen with his own eyes. I believe he had an obligation to express this view, for the learners, as he put it.

His experience is not encouraging for others with something to contribute in a workshop, particularly on the understandably sensitive issue of race.

Beyond the absolute tragedy of Richard Bilkszto, there is another potential victim here: diversity, equity and inclusion (DEI) training. You can already see the outrage brewing: not only are these sessions not worthwhile, they could be dangerous, detractors are saying, using this heartbreaking story as evidence.

This week, Ms. Bildy tweeted: “Many people have silently endured woke struggle sessions in the workplace, and it has felt like an assault on their conscience and humanity. It’s certainly not helping race relations in this country. Time to stop walking on eggshells and find a more unifying approach.”

I sat in briefly on a DEI workshop this week, one focused on Indigenous issues. It was run by a facilitator who was smart, sensitive and serious. The information was hard to take at times, as it should be. And it was eye-opening, as it should be.

DEI training, when done right, is essential. As for Ms. Bildy’s “woke struggle sessions” charge: We need to be awake to the struggles that Black, Indigenous and people of colour people face – experiences that some of us white people have the privilege of not having personally endured.

What’s not okay is if participants are shamed, especially well-meaning people who are doing their best. And trying to make a sincere point – a valid one, according to the lawsuit.

An anti-racism trainer accused of denigrating a Toronto principal who later died by suicide welcomed a review launched by Ontario’s education minister, saying the allegations against her are false and mischaracterize what happened during two training sessions.

Kike Ojo-Thompson, the founder and CEO of a diversity consultancy group – whose listed clients include major corporations, government ministries and national media organizations – said she would co-operate fully with an investigation launched by Minister Stephen Lecce into 2021 sessions she facilitated for the Toronto District School Board.

“We believe the Ministry of Education is best positioned to investigate this matter to get to the bottom of what transpired at the Toronto District School Board after our workshop concluded over two years ago,” Ojo-Thompson wrote in a blog post on the KOJO Institute website Thursday.

Richard Bilkszto filed a lawsuit against the board in April, claiming the session and its aftermath destroyed his reputation. Bilkszto, who continued to pick up TDSB contracts after his 2019 retirement, claims supervisors did not intervene and later retaliated against him when Ojo-Thompson allegedly implied he was racist and humiliated him in front of colleagues after he disagreed that Canada was more racist than the U.S.

None of the allegations have been proven in court and TDSB has not responded directly to the allegations. The board released a statement Thursday saying it hired an outside group to lead an investigation into the circumstances around Bilkszto’s death.

Bilkszto’s lawyer confirmed last week he died by suicide on July 13. He was 60.

His case has since garnered international attention and been seized on by a number of prominent right-wing commentators who have sought to roll back diversity, equity and inclusion initiatives at Canada’s largest school board.

Experts have cautioned against linking suicide to any single circumstance or event.

Ojo-Thompson called Bilkszto’s death a tragedy and extended condolences to his family. She said she only learned about the lawsuit in June, when she was reached for comment by media outlets.

The incident, she said, had been weaponized to discredit and suppress diversity, equity and inclusion work.

“While the coverage by right-wing media of this controversy is disappointing and led to our organization and team members receiving threats and vitriol online, we will not be deterred from our work in building a better society for everyone.”

The lawsuit indicates Bilkszto pushed back when Ojo-Thompson – citing Canada’s failure to reckon with its anti-Black history, its continued celebration of the monarchy, and her own experience living in the United States – said Black people’s experience of racism in the country was worse than in the U.S. Bilkszto, who mentioned his time as a student teacher in Buffalo, disagreed and made reference to Canada’s access to health-care and public education, according to the lawsuit.

He said it would be “an incredible disservice to our learners,” to say Canada was just as bad as the U.S., according to the lawsuit. Ojo-Thompson responded, “we are here to talk about anti-Black racism, but you in your whiteness think that you can tell me what’s really going on for Black people?”

The lawsuit indicates Bilkszto maintained Canada was a more just society, while acknowledging its anti-Black racism. Another KOJO Institute consultant then allegedly stepped in and said the session was not a place to be an apologist for either country.

The lawsuit claims Ojo-Thompson brought up the exchange in a followup session a week later as an example of the ways white supremacy is upheld through resistance.

Bilkszto complained to supervisors the exchanges at the training sessions amounted to workplace harassment, according to the lawsuit. He started a sick leave shortly after the training sessions and was diagnosed with anxiety secondary to a workplace event. A Workplace Safety and Insurance Board case manager accepted his claim of work-related stress and granted loss-of-employment benefits covering about seven weeks, finding he was fit to return to work in July 2021, according to a copy of the WSIB decision provided by his lawyer.

Ojo-Thompson says she was never contacted by the WSIB, despite the case manager concluding her conduct amounted to workplace harassment and bullying.

“Neither Toronto District School Board representatives, nor WSIB adjudicators ever contacted any members of the KOJO team about the false claims being made about our work. It is puzzling that a government agency with adjudicating authority would not consult all named parties to a dispute,” she said in the statement.

After Bilkszto was cleared for work, the lawsuit alleges TDSB “failed or otherwise refused” to reinstate him as principal of an adult learning centre, where he had taught on contract since September 2020, and revoked a separate contract that had been set to start in March.

Reached for comment on Friday, his lawyer Lisa Bildy said she was “not inclined to litigate this case in the media.”

“We have the full recordings of the sessions, which I expect will be released in due course – certainly in the course of the court proceedings, if the family decides to continue with them,” she wrote in an email.

The incident marked a turning point for Bilkszto, according to a statement from his family shared by Bildy last week.

After his experience with the board’s “equity agenda,” the statement says Bilkszto started advocating for a more “equality-focused” approach.

It noted his opposition to TDSB’s recent move to bring in a lottery system, rather than requirements such as test scores or auditions, to admit students to specialized programs and schools in areas such as the arts or athletics. The board says it undertook the change in part to reduce barriers to publicly funded programs and to ensure they reflected the diversity of the city.

Bilkszto also helped found the Toronto chapter of a U.S.-based group that bills itself as a non-partisan civil rights organization that supports a “colour-blindness” approach to race, or what it attempts to recast as “colour-transcendence.” Bildy, a former staff lawyer with the Justice Centre for Constitutional Freedoms who has been outspoken against DEI training, is a member of its advisory board.

The group, Foundation Against Intolerance and Racism, has challenged U.S. universities pursuing affirmative action or race-conscious policies, such as training programs directed at BIPOC teachers.

An anti-racism trainer accused of denigrating a Toronto principal who later died by suicide welcomed a review launched by Ontario’s education minister, saying the allegations against her are false and mischaracterize what happened during two training sessions.

Kike Ojo-Thompson, the founder and CEO of a diversity consultancy group – whose listed clients include major corporations, government ministries and national media organizations – said she would co-operate fully with an investigation launched by Minister Stephen Lecce into 2021 sessions she facilitated for the Toronto District School Board.

“We believe the Ministry of Education is best positioned to investigate this matter to get to the bottom of what transpired at the Toronto District School Board after our workshop concluded over two years ago,” Ojo-Thompson wrote in a blog post on the KOJO Institute website Thursday.

Richard Bilkszto filed a lawsuit against the board in April, claiming the session and its aftermath destroyed his reputation. Bilkszto, who continued to pick up TDSB contracts after his 2019 retirement, claims supervisors did not intervene and later retaliated against him when Ojo-Thompson allegedly implied he was racist and humiliated him in front of colleagues after he disagreed that Canada was more racist than the U.S.

None of the allegations have been proven in court and TDSB has not responded directly to the allegations. The board released a statement Thursday saying it hired an outside group to lead an investigation into the circumstances around Bilkszto’s death.

Bilkszto’s lawyer confirmed last week he died by suicide on July 13. He was 60.

His case has since garnered international attention and been seized on by a number of prominent right-wing commentators who have sought to roll back diversity, equity and inclusion initiatives at Canada’s largest school board.

Experts have cautioned against linking suicide to any single circumstance or event.

Ojo-Thompson called Bilkszto’s death a tragedy and extended condolences to his family. She said she only learned about the lawsuit in June, when she was reached for comment by media outlets.

The incident, she said, had been weaponized to discredit and suppress diversity, equity and inclusion work.

“While the coverage by right-wing media of this controversy is disappointing and led to our organization and team members receiving threats and vitriol online, we will not be deterred from our work in building a better society for everyone.”

The lawsuit indicates Bilkszto pushed back when Ojo-Thompson – citing Canada’s failure to reckon with its anti-Black history, its continued celebration of the monarchy, and her own experience living in the United States – said Black people’s experience of racism in the country was worse than in the U.S. Bilkszto, who mentioned his time as a student teacher in Buffalo, disagreed and made reference to Canada’s access to health-care and public education, according to the lawsuit.

He said it would be “an incredible disservice to our learners,” to say Canada was just as bad as the U.S., according to the lawsuit. Ojo-Thompson responded, “we are here to talk about anti-Black racism, but you in your whiteness think that you can tell me what’s really going on for Black people?”

The lawsuit indicates Bilkszto maintained Canada was a more just society, while acknowledging its anti-Black racism. Another KOJO Institute consultant then allegedly stepped in and said the session was not a place to be an apologist for either country.

The lawsuit claims Ojo-Thompson brought up the exchange in a followup session a week later as an example of the ways white supremacy is upheld through resistance.

Bilkszto complained to supervisors the exchanges at the training sessions amounted to workplace harassment, according to the lawsuit. He started a sick leave shortly after the training sessions and was diagnosed with anxiety secondary to a workplace event. A Workplace Safety and Insurance Board case manager accepted his claim of work-related stress and granted loss-of-employment benefits covering about seven weeks, finding he was fit to return to work in July 2021, according to a copy of the WSIB decision provided by his lawyer.

Ojo-Thompson says she was never contacted by the WSIB, despite the case manager concluding her conduct amounted to workplace harassment and bullying.

“Neither Toronto District School Board representatives, nor WSIB adjudicators ever contacted any members of the KOJO team about the false claims being made about our work. It is puzzling that a government agency with adjudicating authority would not consult all named parties to a dispute,” she said in the statement.

After Bilkszto was cleared for work, the lawsuit alleges TDSB “failed or otherwise refused” to reinstate him as principal of an adult learning centre, where he had taught on contract since September 2020, and revoked a separate contract that had been set to start in March.

Reached for comment on Friday, his lawyer Lisa Bildy said she was “not inclined to litigate this case in the media.”

“We have the full recordings of the sessions, which I expect will be released in due course – certainly in the course of the court proceedings, if the family decides to continue with them,” she wrote in an email.

The incident marked a turning point for Bilkszto, according to a statement from his family shared by Bildy last week.

After his experience with the board’s “equity agenda,” the statement says Bilkszto started advocating for a more “equality-focused” approach.

It noted his opposition to TDSB’s recent move to bring in a lottery system, rather than requirements such as test scores or auditions, to admit students to specialized programs and schools in areas such as the arts or athletics. The board says it undertook the change in part to reduce barriers to publicly funded programs and to ensure they reflected the diversity of the city.

Bilkszto also helped found the Toronto chapter of a U.S.-based group that bills itself as a non-partisan civil rights organization that supports a “colour-blindness” approach to race, or what it attempts to recast as “colour-transcendence.” Bildy, a former staff lawyer with the Justice Centre for Constitutional Freedoms who has been outspoken against DEI training, is a member of its advisory board.

The group, Foundation Against Intolerance and Racism, has challenged U.S. universities pursuing affirmative action or race-conscious policies, such as training programs directed at BIPOC teachers.

Rebecca Paulhus has been selected as the new principal of North Attleborough Middle School. (Photo courtesy North Attleborough Public Schools)

NORTH ATTLEBOROUGH – Superintendent John Antonucci is pleased to announce that Rebecca (Fisher) Paulhus has been selected as the new principal of North Attleborough Middle School.

Paulhus will begin in the position on August 7, 2023.

Paulhus, a North Attleborough native, was selected following a comprehensive search and interview process that included input from multiple stakeholders, including North Attleborough Middle School faculty and staff, parents, community members and administrators.

“I am very excited to welcome Becky to our school community. She is a proven leader, she is student-centered, and she has exceptional interpersonal skills. She has a track record of fostering a warm, welcoming, and inclusive school culture, and I have no doubt she is a great fit for the Middle School,” said Superintendent Antonucci.

Paulhus comes from Weymouth Public Schools, where she has served in a variety of capacities since 2013. Most recently, Paulhus served as the Associate Principal of Weymouth Middle School and High School.

While at Weymouth Public Schools, she participated in the School Council Crisis Team, oversaw the Student Intervention Team, and all tiered interventions, services and staff. During this time Paulhus also served as Dean of Students and as a Special Education Team Chairperson.

Prior to her career in Weymouth, Paulhus served as a middle school teacher and athletic coach for North Attleborough Public Schools from 2007 to 2013.

“I am so incredibly honored to be the Principal of North Attleborough Middle School. I am aware of the history embedded in the town, the school, and the traditions that continue the legacy of service, scholar, arts, and athletics in such ways as Hoops for Hearts and Unified Sport,” said Paulhus.

Paulhus holds a master’s degree in Special Education and bachelor’s degree in Sociology and Special Education from Bridgewater State University and a Certificate of Advanced Graduate Studies from American International College.

“The opportunity to give back to a community that I was raised in, where I was educated, and where I spent many, many years coaching and teaching is something I could not pass up,” said Paulhus. “I am excited to get the school year started!”

Rebecca Paulhus has been selected as the new principal of North Attleborough Middle School. (Photo courtesy North Attleborough Public Schools)

NORTH ATTLEBOROUGH – Superintendent John Antonucci is pleased to announce that Rebecca (Fisher) Paulhus has been selected as the new principal of North Attleborough Middle School.

Paulhus will begin in the position on August 7, 2023.

Paulhus, a North Attleborough native, was selected following a comprehensive search and interview process that included input from multiple stakeholders, including North Attleborough Middle School faculty and staff, parents, community members and administrators.

“I am very excited to welcome Becky to our school community. She is a proven leader, she is student-centered, and she has exceptional interpersonal skills. She has a track record of fostering a warm, welcoming, and inclusive school culture, and I have no doubt she is a great fit for the Middle School,” said Superintendent Antonucci.

Paulhus comes from Weymouth Public Schools, where she has served in a variety of capacities since 2013. Most recently, Paulhus served as the Associate Principal of Weymouth Middle School and High School.

While at Weymouth Public Schools, she participated in the School Council Crisis Team, oversaw the Student Intervention Team, and all tiered interventions, services and staff. During this time Paulhus also served as Dean of Students and as a Special Education Team Chairperson.

Prior to her career in Weymouth, Paulhus served as a middle school teacher and athletic coach for North Attleborough Public Schools from 2007 to 2013.

“I am so incredibly honored to be the Principal of North Attleborough Middle School. I am aware of the history embedded in the town, the school, and the traditions that continue the legacy of service, scholar, arts, and athletics in such ways as Hoops for Hearts and Unified Sport,” said Paulhus.

Paulhus holds a master’s degree in Special Education and bachelor’s degree in Sociology and Special Education from Bridgewater State University and a Certificate of Advanced Graduate Studies from American International College.

“The opportunity to give back to a community that I was raised in, where I was educated, and where I spent many, many years coaching and teaching is something I could not pass up,” said Paulhus. “I am excited to get the school year started!”

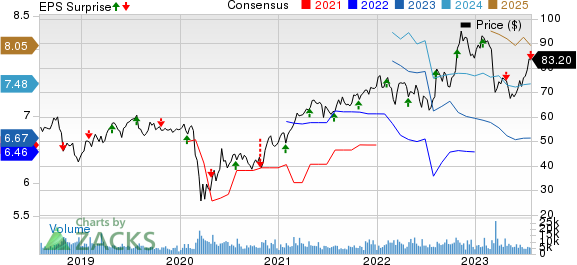

Principal Financial Group, Inc.’s PFG second-quarter 2023 operating net income of $1.53 per share missed the Zacks Consensus Estimate by 7.8%. Also, the bottom line decreased 7.3% year over year.

Operating revenues increased 11.5% year over year to $3.5 billion due to increased premiums and other considerations. The metric surpassed the Zacks Consensus Estimate by 0.3%.

Principal Financial witnessed soft performance across most segments and higher expenses, offset by improving asset under management (AUM) and higher revenues in Retirement and Income Solution and Benefits and Protection businesses.

Principal Financial Group, Inc. Price, Consensus and EPS Surprise

Principal Financial Group, Inc. Price, Consensus and EPS Surprise

Principal Financial Group, Inc. price-consensus-eps-surprise-chart | Principal Financial Group, Inc. Quote

Behind the Headlines

Total expenses increased 15.2% year over year to $3.1 billion due to higher benefits, claims and settlement expenses. The figure was higher than our estimate of $3 billion.

As of Jun 30, 2023, Principal Financial’s AUM amounted to $674 billion, up 6.7% year over year.

Segment Update

Retirement and Income Solution: Revenues increased 27% year over year to $1.7 billion because of higher premiums and other considerations, fees and net investment income. The figure beat our estimate by 6.3%.

Pre-tax operating earnings decreased 8.8% year over year to $232.3 million, primarily due to lower net revenues.

Principal Global Investors: Revenues of $390.1 million were down 15.9% from the prior-year quarter due to lower fees and other revenues.

Pre-tax operating earnings decreased 30.6% year over year to $125 million due to lower operating revenues less pass-through expenses.

Principal International: Revenues decreased 32% year over year to $302.3 million in the quarter due to lower premiums and other considerations and net investment income.

Pre-tax operating earnings decreased 29.3% year over year to $63.2 million, driven by lower combined net revenues. The figure lagged our estimate by 20%.

Benefits and Protection: Revenues increased 24.6% year over year to $1.1 billion owing to higher net investment income, fees and other revenues. The metric lagged our estimate by a whisker.

Pre-Tax operating earnings of $124.9 million decreased 20.7% year over year, mainly due to lower net investment income in the Life Insurance business. The metric lagged our estimate by 19.9%.

Corporate: Operating loss of $97.4 million was narrower than $152.9 million loss incurred a year ago. This decrease was due to higher net investment income. The figure was narrower than our estimate of a loss of $106.4 million.

Financial Update

As of Jun 30, 2023, cash and cash equivalents were $4,073.9 million, down from $4,848 million at 2022-end.

At the second-quarter end, debt was $3,992.9 billion, down from $3,997 million at 2022-end. As of Jun 30, 2023, book value per share (excluding AOCI other than foreign currency translation adjustment) was $52.45, up from $50.92 at 2022-end.

Dividend and Share Repurchase Update

Principal Financial paid out $154.9 million in dividends and deployed $100 million to buy back 1.4 million shares in the second quarter.

The board of directors declared third-quarter dividend of 65 cents per share, 2% higher than the previous dividend of 64 cents. The dividend will be paid out on Sep 29, 2023, to shareholders of record as of Sep 7.

Zacks Rank

Principal Financial currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Other Finance Sector Releases

Of the other Finance sector players that have reported second-quarter results so far, the bottom-line results of Synchrony Financial SYF, American Express Company AXP and Morgan Stanley MS beat the respective Zacks Consensus Estimate.

Synchrony Financial reported second-quarter 2023 adjusted earnings per share (EPS) of $1.32, which beat the Zacks Consensus Estimate of $1.22. However, the bottom line plunged 17.5% year over year. Net interest income of SYF improved 8.4% year over year to $4,120 million, beating the consensus mark by 0.6%.

Other income of Synchrony Financial amounted to $61 million, which dropped 69.2% year over year in the second quarter. Total loan receivables grew 14.7% year over year to $94.8 billion. The purchase volume advanced 0.1% year over year to $47,276 million in the second quarter.

American Express reported second-quarter 2023 EPS of $2.89, beating the Zacks Consensus Estimate by 3.2%. The bottom line increased 12.5% year over year. For the quarter under review, AXP’s total revenues, net of interest expense, increased 12.4% year over year to $15,054 million.

However, the top line missed the consensus estimate by 2.3%. Network volumes jumped 8% year over year to $426.6 billion in the second quarter. Total interest income was $4,775 million in the second quarter, up 71% year over year. The International Card Services segment recorded a pre-tax income of $253 million, up 38% from a year ago.

Morgan Stanley’s second-quarter 2023 EPS of $1.24 surpassed the Zacks Consensus Estimate of earnings of $1.14 per share. However, the bottom line reflects a decline of 11% from the year-ago quarter. Net revenues were $13.46 billion, up 2% from the prior-year quarter.

The top line beat the consensus estimate of $12.76 billion. While equity and fixed income underwriting fees increased 52% and 21%, respectively, from the prior-year quarter, advisory fees declined 24%. Therefore, total investment banking fees increased only marginally from the prior-year quarter. Fixed-income trading revenues of MS decreased 31%, and equity trading income declined 14% year over year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Declares increase to third quarter 2023 common stock dividend

Company Highlights

Second quarter 2023 net income attributable to Principal Financial Group®, Inc. (PFG)1 of $389 million, or $1.58 per diluted share, includes $64 million of income from exited business.

Second quarter 2023 non-GAAP operating earnings2 of $376 million, or $1.53 per diluted share.

Returned $255 million of capital to shareholders in second quarter 2023.

Company declares third quarter 2023 common stock dividend of $0.65 per share, a 1 cent or 2% increase over second quarter 2023.

Assets under management (AUM) of $674 billion, which is included in assets under administration (AUA) of $1.5 trillion.

DES MOINES, Iowa, July 27, 2023--(BUSINESS WIRE)--Principal Financial Group® (Nasdaq: PFG) announced results for second quarter 2023.

Non-GAAP net income attributable to PFG excluding income from exited business1 for second quarter 2023 of $324.5 million, compared to $207.7 million for second quarter 2022. Non-GAAP net income excluding income from exited business per diluted share of $1.32 for second quarter 2023.

Non-GAAP operating earnings for second quarter 2023 of $375.8 million, compared to $424.0 million for second quarter 2022. Non-GAAP operating earnings per diluted share of $1.53 for second quarter 2023 compared to $1.65 per diluted share for second quarter 2022.

Quarterly common stock dividend of $0.65 per share for third quarter 2023 was authorized by the company’s Board of Directors, bringing the trailing twelve-month dividend to $2.57 per share. The dividend will be payable on September 29, 2023, to shareholders of record as of September 7, 2023.

"Our integrated business model and leading position in the small to mid-sized business segment contributed to healthy growth across our Benefits and Protection and U.S. Retirement businesses as well as strong second quarter results with non-GAAP operating earnings of $376 million. We returned over $250 million to our shareholders during the quarter and remain confident in our full-year guidance," said Dan Houston, chairman, president, and CEO of Principal®. "

"Despite pressured net cash flow in the quarter, we have momentum going into the remainder of 2023, particularly within global asset management. With markets recovering, we expect greater opportunities to capture assets in our actively managed solutions in the second half of the year. Investment performance rebounded significantly across many of our solutions in the second quarter, and we’re confident we have the right capabilities to meet client needs and deliver long-term net cash flows."

Second quarter highlights

Strong Morningstar investment performance3 with 71% of Principal investment options above median on a one-year basis, 62% on a three-year basis, 76% on a five-year basis, and 85% on a ten-year basis

Retirement and Income Solutions (RIS) operating margin4 of 36%; sales of $5.5 billion, including $0.6 billion of pension risk transfer sales

Principal Global Investors (PGI) managed AUM of $485.8 billion; operating margin5 of 35%

Principal International (PI) reported AUM of $174.4 billion, up 17% from second quarter 2022

Specialty Benefits premium and fees increased 8% from second quarter 2022 driven by continued strong sales, retention, employment and wage growth

Life Insurance sales increased 28% from second quarter 2022

Returned $254.9 million of capital to shareholders during the second quarter, including:

$100.0 million to repurchase 1.4 million shares of common stock; and

$154.9 million of common stock dividends with the $0.64 per share common dividend paid in the second quarter

Retired $700.0 million of long-term debt during the quarter, using the proceeds from issuances in first quarter 2023

Strong financial position

Segment Results

Retirement and Income Solutions

(in millions except percentages or otherwise noted)

Quarter

Trailing Twelve Months

2Q23

2Q22

% Change

2Q23

2Q22

% Change

Pre-tax operating earnings6

$232.3

$254.6

(9)%

$892.4

$1,031.9

(14)%

Net revenue7

$639.9

$651.7

(2)%

$2,522.3

$2,784.3

(9)%

Operating margin

36.3%

39.1%

35.4%

37.1%

Pre-tax operating earnings decreased $22.3 million primarily due to lower net revenue.

Net revenue decreased $11.8 million primarily due to lower variable investment income, which was partially offset by the benefits of rising interest rates. Additionally, the prior year quarter was adversely impacted by the 2022 reinsurance transaction.

Principal Global Investors

(in millions except percentages or otherwise noted)

Quarter

Trailing Twelve Months

2Q23

2Q22

% Change

2Q23

2Q22

% Change

Pre-tax operating earnings

$125.0

$180.0

(31)%

$514.7

$706.3

(27)%

Operating revenues less pass-through expenses8

$359.6

$428.7

(16)%

$1,473.7

$1,703.4

(13)%

Operating margin

34.9%

42.3%

35.2%

41.8%

Total PGI assets under management (billions)

$485.8

$469.8

3%

PGI sourced assets under management (billions)

$249.8

$243.7

3%

Pre-tax operating earnings decreased $55.0 million primarily due to lower operating revenues less pass-through expenses.

Operating revenues less pass-through expenses decreased $69.1 million primarily due to lower performance fees as well as lower management fees from a decrease in average AUM.

Principal International

(in millions except percentages or otherwise noted)

Quarter

Trailing Twelve Months

2Q23

2Q22

% Change

2Q23

2Q22

% Change

Pre-tax operating earnings

$63.2

$89.4

(29)%

$283.6

$359.1

(21)%

Combined net revenue (at PFG share)9

$229.4

$244.8

(6)%

$921.8

$1,011.4

(9)%

Operating margin10

27.6%

36.5%

30.8%

35.5%

Assets under management (billions)

$174.4

$148.9

17%

Pre-tax operating earnings decreased $26.2 million primarily due to lower combined net revenue.

Combined net revenue (at PFG share) decreased $15.4 million primarily due to lower variable investment income and unfavorable impacts from inflation and LDTI discount rate movements, partially offset by growth in the business.

Specialty Benefits

(in millions except percentages or otherwise noted)

Quarter

Trailing Twelve Months

2Q23

2Q22

% Change

2Q23

2Q22

% Change

Pre-tax operating earnings

$98.1

$86.8

13%

$441.6

$266.3

66%

Premium and fees

$750.2

$695.0

8%

$2,927.8

$2,660.5

10%

Operating margin11

13.1%

12.5%

15.1%

10.0%

Incurred loss ratio

62.0%

65.2%

59.5%

66.4%

Pre-tax operating earnings increased $11.3 million due to growth in the business and a decrease in the incurred loss ratio, partially offset by lower net investment income.

Premium and fees increased $55.2 million driven by strong sales, retention, employment and wage growth.

Incurred loss ratio decreased primarily due to lower group life mortality and improved disability experience.

Life Insurance

(in millions except percentages or otherwise noted)

Quarter

Trailing Twelve Months

2Q23

2Q22

% Change

2Q23

2Q22

% Change

Pre-tax operating earnings (losses)

$26.8

$70.8

(62)%

$102.5

$156.1

(34)%

Premium and fees

$229.0

$130.6

75%

$913.2

$1,090.7

(16)%

Pre-tax return on premium and fees

11.7%

54.2%

11.2%

14.3%

Pre-tax operating earnings decreased $44.0 million primarily due to lower net investment income. Additionally, the prior year quarter was impacted by the 2022 reinsurance transactions.

Premium and fees increased $98.4 million as a result of the impacts of the 2022 reinsurance transactions in the prior year quarter.

Corporate

(in millions except percentages or otherwise noted)

Quarter

Trailing Twelve Months

2Q23

2Q22

% Change

2Q23

2Q22

% Change

Pre-tax operating losses

$(97.4)

$(152.9)

36%

$(381.0)

$(473.4)

20%

Forward looking and cautionary statements

Certain statements made by the company which are not historical facts may be considered forward-looking statements, including, without limitation, statements as to non-GAAP operating earnings, net income attributable to PFG, net cash flow, realized and unrealized gains and losses, capital and liquidity positions, sales and earnings trends, and management’s beliefs, expectations, goals and opinions. The company does not undertake to update these statements, which are based on a number of assumptions concerning future conditions that may ultimately prove to be inaccurate. Future events and their effects on the company may not be those anticipated, and actual results may differ materially from the results anticipated in these forward-looking statements. The risks, uncertainties and factors that could cause or contribute to such material differences are discussed in the company’s annual report on Form 10-K for the year ended Dec. 31, 2022, and in the company’s quarterly report on Form 10-Q for the quarter ended Mar. 31, 2023, filed by the company with the U.S. Securities and Exchange Commission, as updated or supplemented from time to time in subsequent filings. These risks and uncertainties include, without limitation: adverse capital and credit market conditions may significantly affect the company’s ability to meet liquidity needs, access to capital and cost of capital; conditions in the global capital markets and the economy generally; volatility or declines in the equity, bond or real estate markets; changes in interest rates or credit spreads or a prolonged low interest rate environment; the elimination of the London Inter-Bank Offered Rate ("LIBOR"); the company’s investment portfolio is subject to several risks that may diminish the value of its invested assets and the investment returns credited to customers; the company’s valuation of investments and the determination of the amount of allowances and impairments taken on such investments may include methodologies, estimations and assumptions that are subject to differing interpretations; any impairments of or valuation allowances against the company’s deferred tax assets; the company’s actual experience for insurance and annuity products could differ significantly from its pricing and reserving assumptions; the pattern of amortizing the company’s DAC asset and other actuarial balances may change; changes in laws, regulations or accounting standards; the company’s ability to pay stockholder dividends, make share repurchases and meet its obligations may be constrained by the limitations on dividends or other distributions Iowa insurance laws impose on Principal Life; litigation and regulatory investigations; from time to time the company may become subject to tax audits, tax litigation or similar proceedings, and as a result it may owe additional taxes, interest and penalties in amounts that may be material; applicable laws and the company’s certificate of incorporation and by-laws may discourage takeovers and business combinations that some stockholders might consider in their best interests; competition, including from companies that may have greater financial resources, broader arrays of products, higher ratings and stronger financial performance; a downgrade in the company’s financial strength or credit ratings; client terminations, withdrawals or changes in investor preferences; the company’s hedging or risk management strategies prove ineffective or insufficient; international business risks; risks arising from participation in joint ventures; the company may need to fund deficiencies in its "Closed Block" assets; the company’s reinsurers could default on their obligations or increase their rates; risks arising from acquisitions of businesses; risks related to administering reinsurance transactions; a pandemic, terrorist attack, military action or other catastrophic event; global climate change; technological and societal changes may disrupt the company’s business model and impair its ability to retain existing customers, attract new customers and maintain its profitability; damage to the company’s reputation; the company may not be able to protect its intellectual property and may be subject to infringement claims; inability to attract, develop and retain qualified employees and sales representatives and develop new distribution sources; an interruption in information technology, infrastructure or other internal or external systems used for business operations, or a failure to maintain the confidentiality, integrity or availability of data residing on such systems; loss of key vendor relationships or failure of a vendor to protect information of our customers or employees; and the company’s enterprise risk management framework may not be fully effective in identifying or mitigating all of the risks to which the company is exposed.

Use of Non-GAAP financial measures

The company uses a number of non-GAAP financial measures that management believes are useful to investors because they illustrate the performance of normal, ongoing operations, which is important in understanding and evaluating the company’s financial condition and results of operations. They are not, however, a substitute for U.S. GAAP financial measures. Therefore, the company has provided reconciliations of the non-GAAP measures to the most directly comparable U.S. GAAP measure at the end of the release. The company adjusts U.S. GAAP measures for items not directly related to ongoing operations. However, it is possible these adjusting items have occurred in the past and could recur in future reporting periods. Management also uses non-GAAP measures for goal setting, as a basis for determining employee and senior management awards and compensation and evaluating performance on a basis comparable to that used by investors and securities analysts.

Earnings conference call

On Friday, Jul. 28, 2023, at 10:00 a.m. (ET), Chairman, President and Chief Executive Officer Dan Houston and Executive Vice President and Chief Financial Officer Deanna Strable will lead a discussion of results and the impacts on future prospects, asset quality and capital adequacy during a live conference call, which can be accessed as follows:

Via live Internet webcast. Please go to investors.principal.com at least 10-15 minutes prior to the start of the call to register, and to download and install any necessary audio software.

Via telephone by dialing 877-407-0832 (U.S. and Canadian callers) or 201-689-8433 (international callers) approximately 10 minutes prior to the start of the call.

Replay of the earnings call via webcast as well as a transcript of the call will be available after the call at investors.principal.com.

The company’s financial supplement and slide presentation is currently available at investors.principal.com, and may be referred to during the call.

Principal Financial Group® (Nasdaq: PFG) is a global financial company with approximately 19,000 employees13 passionate about improving the wealth and well-being of people and businesses. In business for more than 140 years, we’re helping approximately 62 million customers13 plan, insure, invest, and retire, while working to improve our planet, support the communities where we do business, and build a diverse, inclusive workforce. Principal® is proud to be recognized as one of the 2023 World’s Most Ethical Companies14, a member of the Bloomberg Gender Equality Index, and a Top 10 "Best Places to Work in Money Management15." Learn more about Principal and our commitment to sustainability, inclusion, and purpose at principal.com.

Summary of Principal Financial Group, Inc. and Segment Results

Principal Financial Group, Inc. Results:

(in millions)

Three Months Ended,

Trailing Twelve Months,

6/30/23

6/30/22

6/30/23

6/30/22

Net income (loss) attributable to PFG

$

388.8

$

3,118.7

$

1,548.2

$

4,209.1

(Income) loss from exited business

(64.3

)

(2,911.0

)

30.0

(2,911.0

)

Net income (loss) attributable to PFG excluding exited business

$

324.5

$

207.7

$

1,578.2

$

1,298.1

Net realized capital (gains) losses, as adjusted

51.3

216.3

(38.0

)

357.1

Non-GAAP Operating Earnings*

$

375.8

$

424.0

$

1,540.2

$

1,655.2

Income taxes

72.2

104.7

313.6

391.1

Non-GAAP Pre-Tax Operating Earnings

$

448.0

$

528.7

$

1,853.8

$

2,046.3

Segment Pre-Tax Operating Earnings (Losses):

Retirement and Income Solutions

$

232.3

$

254.6

$

892.4

$

1,031.9

Principal Asset Management

188.2

269.4

798.3

1,065.4

Benefits and Protection

124.9

157.6

544.1

422.4

Corporate

(97.4

)

(152.9

)

(381.0

)

(473.4

)

Total Segment Pre-Tax Operating Earnings

$

448.0

$

528.7

$

1,853.8

$

2,046.3

Per Diluted Share

Three Months Ended,

Six Months Ended,

6/30/23

6/30/22

6/30/23

6/30/22

Net income (loss)

$

1.58

$

12.17

$

1.01

$

13.30

(Income) loss from exited business

(0.26

)

(11.36

)

1.72

(11.20

)

Net income (loss) excluding exited business

$

1.32

$

0.81

$

2.73

$

2.10

Net realized capital (gains) losses, as adjusted

0.21

0.84

0.28

1.06

Non-GAAP Operating Earnings

$

1.53

$

1.65

$

3.01

$

3.16

Weighted-average diluted common shares outstanding(in millions)

245.5

256.3

246.4

260.0

*U.S. GAAP (GAAP) net income attributable to PFG versus non-GAAP operating earnings

Management uses non-GAAP operating earnings, which is a financial measure that excludes the effect of net realized capital gains and losses, as adjusted, income (loss) from exited business and other after-tax adjustments the company believes are not indicative of overall operating trends, for goal setting, as a basis for determining employee and senior management awards and compensation and evaluating performance on a basis comparable to that used by investors and securities analysts. Note: it is possible these adjusting items have occurred in the past and could recur in future reporting periods. While these items may be significant components in understanding and assessing our consolidated financial performance, management believes the presentation of non-GAAP operating earnings enhances the understanding of results of operations by highlighting earnings attributable to the normal, ongoing operations of the company’s businesses.

Selected Balance Sheet Statistics

Period Ended,

6/30/23

12/31/22

Total assets (in billions)

$

299.2

$

290.6

Stockholders’ equity (in millions)

$

10,389.5

$

10,017.8

Total common equity (in millions)

$

10,344.5

$

9,976.7

Total common equity excluding cumulative change in fair value of funds withheld embedded derivative and accumulated other comprehensive income (AOCI) other than foreign currency translation adjustment (in millions)

$

12,693.8

$

12,398.5

End of period common shares outstanding (in millions)

242.0

243.5

Book value per common share

$

42.75

$

40.97

Book value per common share excluding cumulative change in fair value of funds withheld embedded derivative and AOCI other than foreign currency translation adjustment

$

52.45

$

50.92

Principal Financial Group, Inc.

Reconciliation of U.S. GAAP to Non-GAAP Financial Measures

(in millions, except as indicated)

Period Ended,

6/30/23

12/31/22

Stockholders’ Equity, Excluding AOCI Other Than Foreign Currency Translation Adjustment, Available to Common Stockholders:

Stockholders’ equity

$

10,389.5

$

10,017.8

Noncontrolling interest

(45.0

)

(41.1

)

Stockholders’ equity available to common stockholders

10,344.5

9,976.7

Cumulative change in fair value of funds withheld embedded derivative

(2,464.8

)

(2,885.6

)

AOCI, other than foreign currency translation adjustment

4,814.1

5,307.4

Stockholders’ equity, excluding AOCI other than cumulative change in fair value of funds withheld embedded derivative and foreign currency translation adjustment, available to common stockholders

$

12,693.8

$

12,398.5

Book Value Per Common Share, Excluding AOCI Other Than Foreign Currency Translation Adjustment:

Book value per common share

$

42.75

$

40.97

Cumulative change in fair value of funds withheld embedded derivative and AOCI, other than foreign currency translation adjustment

9.70

9.95

Book value per common share, excluding AOCI other than foreign currency translation adjustment

$

52.45

$

50.92

Principal Financial Group, Inc.

Reconciliation of U.S. GAAP to Non-GAAP Financial Measures

(in millions)

Three Months Ended,

Trailing Twelve Months,

6/30/23

6/30/22

6/30/23

6/30/22

Income Taxes:

Total GAAP income taxes (benefit)

$

59.9

$

836.7

$

299.5

$

1,014.7

Net realized capital gains (losses) tax adjustments

12.7

69.3

(9.9

)

130.6

Exited business tax adjustments

(17.1

)

(813.5

)

(38.7

)

(813.5

)

Income taxes related to equity method investments and noncontrolling interest

16.7

12.2

62.7

59.3

Income taxes

$

72.2

$

104.7

$

313.6

$

391.1

Net Realized Capital Gains (Losses):

GAAP net realized capital gains (losses)

$

(72.8

)

$

(189.4

)

$

5.1

$

(332.4

)

Market value adjustments to fee revenues

0.2

0.1

0.8

(0.1

)

Net realized capital gains (losses) related to equity method investments

8.1

(9.0

)

5.9

(29.1

)

Derivative and hedging-related revenue adjustments

(5.0

)

(25.0

)

(37.2

)

(123.7

)

Certain variable annuity fees

18.4

19.1

73.6

80.5

Sponsored investment fund adjustments

5.7

5.9

22.3

22.9

Capital gains distributed – operating expenses

(7.3

)

35.0

17.5

70.1

Amortization of actuarial balances

0.1

(6.7

)

0.1

(0.1

)

Derivative and hedging-related expense adjustments

0.1

-

0.1

-

Market value adjustments of embedded derivatives

5.3

(20.2

)

4.0

(43.8

)

Market value adjustments of market risk benefits

(4.4

)

(113.9

)

(31.5

)

(156.3

)

Capital gains distributed – cost of interest credited

(9.5

)

(5.4

)

(0.1

)

(2.9

)

Net realized capital gains (losses) tax adjustments

12.7

69.3

(9.9

)

130.6

Net realized capital gains (losses) attributable to noncontrolling interest, after-tax

(2.9

)

23.9

(12.7

)

27.2

Total net realized capital gains (losses) after-tax adjustments

21.5

(26.9

)

32.9

(24.7

)

Net realized capital gains (losses), as adjusted

$

(51.3

)

$

(216.3

)

$

38.0

$

(357.1

)

Income (Loss) from Exited Business:

Pre-tax impacts of exited business:

Strategic review costs and impacts

$

-

$

64.0

$

(23.6

)

$

64.0

Amortization of reinsurance gains (losses)

(20.3

)

(30.5

)

(68.6

)

(30.5

)

Other impacts of reinsured business

(30.0

)

(65.3

)

(131.1

)

(65.3

)

Net realized capital gains (losses) on funds withheld assets

37.8

689.0

179.2

689.0

Change in fair value of funds withheld embedded derivative

93.9

3,067.3

52.8

3,067.3

Tax impacts of exited business

(17.1

)

(813.5

)

(38.7

)

(813.5

)

Total income (loss) from exited business

$

64.3

$

2,911.0

$

(30.0

)

$

2,911.0

Principal Financial Group, Inc.

Reconciliation of U.S. GAAP to Non-GAAP Financial Measures

(in millions)

Three Months Ended,

Trailing Twelve Months,

6/30/23

6/30/22

6/30/23

6/30/22

Principal Global Investors Operating Revenues Less Pass-Through Expenses:

Operating revenues

$

390.1

$

463.6

$

1,599.4

$

1,858.0

Commissions and other expenses

(30.5

)

(34.9

)

(125.7

)

(154.6

)

Operating revenues less pass-through expenses

$

359.6

$

428.7

$

1,473.7

$

1,703.4

Principal International Combined Net Revenue (at PFG Share)

Pre-tax operating earnings

$

63.2

$

89.4

$

283.6

$

359.1

Combined operating expenses other than pass-through commissions (at PFG share)

166.2

155.4

638.2

652.3

Combined net revenue (at PFG share)

$

229.4

$

244.8

$

921.8

$

1,011.4

1 All financial results and periods reflect the adoption of long-duration targeted improvements (LDTI) accounting guidance.

2 Use of non-GAAP financial measures is discussed in this release after segment results. Non-GAAP operating earnings for total company is after tax.

3 Represents the percentage of Principal actively managed mutual funds, exchange traded funds (ETFs), insurance separate accounts, and collective investment trusts (CITs) in the top two Morningstar quartiles. Excludes Money Market, Stable Value, Liability Driven Investment, Hedge Fund Separate Account and U.S. Property Separate Account.

4 Operating margin for RIS = pre-tax operating earnings divided by net revenue.

5 Operating margin for PGI = pre-tax operating earnings, adjusted for noncontrolling interest divided by operating revenues less pass-through expenses.

6 Pre-tax operating earnings = operating earnings before income taxes and after noncontrolling interest.

7 Net revenue = operating revenues less: benefits, claims and settlement expenses; liability for future policy benefits remeasurement (gain) loss; market risk benefit remeasurement (gain) loss; and dividends to policyholders.

8 The company has provided reconciliations of the non-GAAP measures to the most directly comparable U.S. GAAP measures at the end of the release. The company has determined this measure is more representative of underlying operating revenues growth for PGI as it removes commissions and other expenses that are collected through fee revenue and passed through expenses with no impact to pre-tax operating earnings.

9 Combined net revenue (a non-GAAP financial measure): net revenue for all PI companies at 100% less pass-through commissions. The company has determined combined net revenue (at PFG share) is more representative of underlying net revenue growth for PI as it reflects our proportionate share of consolidated and equity method subsidiaries. In addition, using this net revenue metric provides a more meaningful representation of our operating margin.

10 Operating margin for PI = pre-tax operating earnings divided by combined net revenue (at PFG share).

11 Operating margin for Benefits and Protection = pre-tax operating earnings divided by premium and fees.

12 Principal, Principal and symbol design and Principal Financial Group are trademarks and service marks of Principal Financial Services, Inc., a member of the Principal Financial Group.

:format(jpeg)/cloudfront-us-east-1.images.arcpublishing.com/tgam/GGQKLO4CPVB27J7SI44YFWMLCY.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/tgam/FMAG3HARDBKBPDZ74LPT5HFWXQ.jpg)